Your Social Security Sweet SpotI’m not a financial advisor or tax accountant and I’ve never sold any kind of financial securities. I’m just a math and computer geek who has done a lot of analysis of stock market risk and taxes to prepare for retirement. I’m not selling anything and I don’t want any of your financial information. I just want to share my analysis work with others! That said, use the information you see here at your own risk!

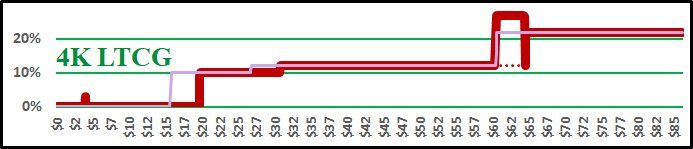

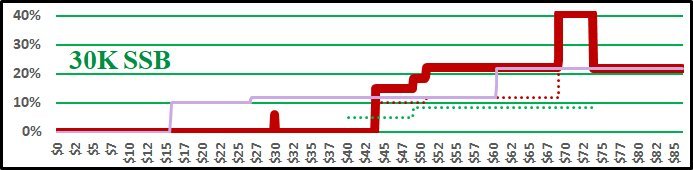

Let’s start this conversation by looking at Marginal Tax Rates, the percentage of the Next Dollar of income that goes to the IRS as Federal Taxes. Since we are talking about retirement, all of these example are for individuals with standard deductions over the age of 65.  We are all familiar with the standard federal tax brackets of 10%, 12%, 22%, etcetera, but what if you also had $4,000 of Long Term Capital Gains?  This tax line starts later because your Long Term Capital Gains are Tax Delayed income. Your LTCGs are initially tax free income, then at the gross income point $100 before they would normally be pushed into the 22% tax bracket, these gains slowly become taxable, at a 15% tax rate, at the same time as the standard income that is making them taxable is also being taxes at 12%. You pay 12% on the normal income plus 15% on the capital gains which results in a Marginal Tax Rate of 27%. Now let’s look at our Social Security Benefits which are also Tax Delayed income. The benefit level in the next chart will be $2,500 monthly, $30,000 yearly. That is the benefit level that you would receive if your average inflation adjusted income was about $53,000 and you started your benefits 3 years after your full retirement age or a $72,000 income if you started your benefits at your full retirement age.  $30,000 of Tax Delayed income really pushes the start of the red marginal tax line to a much higher gross income level. The dotted green line shows were your Social Security benefits slowly becomes taxable income at, the dotted red line, your normal Tax Brackets, first at 50 cents per extra dollar of income, then at 85 cents per extra dollar of income until 85% of your benefits have become taxable income as reported on line 5, entry 5b, on your 1040 Federal Tax Return.

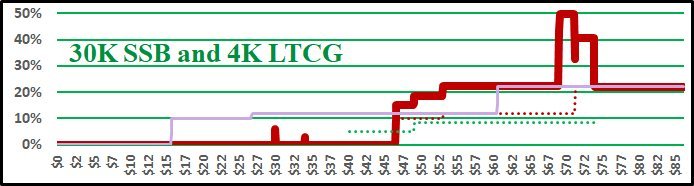

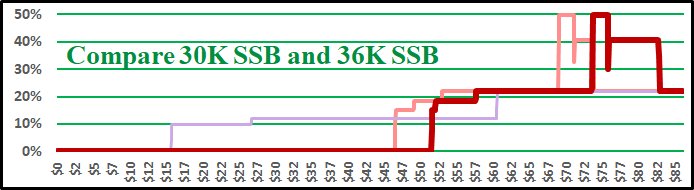

This graph illustrates your marginal tax rates when you have $4,000 of LTCGs and $30,000 of SSB. The taxes paid on the first $66,770 of gross income is only $4,315, which is an Effective Tax Rate, total tax over total income, of only 6.46%. The Marginal Tax Rates over the next $6,936 of gross income are triple taxed at 49.95% then double taxed at 40.7% for a total Federal Tax of $3,013 which is an overall tax rate of 43.44% within your Personal Marginal Tax Hump.  This final graph is the focus of this entire website. When you increase your Social Security benefit level from $30,000 to $36,000, $500 a month more, Your Personal pre-hump gross income level, Your Personal Sweet Spot, increased from $66,770 to $71,392 while the taxes paid on that amount remained at $4,315 which lowered your effective pre-hump tax rate to 6.04%, while the size of Your Personal Tax Hump also increased from $6,936 to $11,314.

Compared to the pre-retirement cost of Roth contributions or conversions; the extra cost of doing the withdraw during retirement while below your Sweet Spot at your Marginal 22.2% Tax Rate is only 3 or 4 dollars, so keep the money in your Roth for when it is really needed. But, if your income needs are pushing you beyond your Sweet Spot into your Personal Tax Hump a single $1,000 will cost you hundreds of extra tax dollars, and if you need a few thousand for a medical bill, new furniture, a home repair, or a nice vacation, your cost can easily grow into thousands of extra tax dollars. That is why one of our topics will be doing Roth Conversions prior to your actual retirement date! Having a source of Tax Free income during retirement is always a good idea! Be prepared, don’t be scared! You may be tempted to jump around to the different pages of this website, but if you do, you might miss the entire concept, so please follow the “next page” links at the bottom of each page. During your journey we will explain:

Now let’s move on to see how your personal marital status, your personal SS benefit level, and your personal investments change your Personal Marginal Tax Brackets! Next - Let's take a closer look at the Hump! |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||